AI Agents Can Spend Money. Enterprise Controls Can't Keep Up

Something changed quietly in enterprise software over the last two years. AI agents — autonomous software systems that can reason, plan, and take action — gained access to real money.

Not hypothetical money. Not sandboxed test environments. Real corporate cards, real vendor accounts, real payment rails. Procurement bots are renewing SaaS contracts. Expense agents are booking travel. Accounts payable workflows are paying invoices. AI systems are doing all of this autonomously, around the clock, without a human signing off on each transaction.

This is the promise of agentic AI: genuine automation of high-volume, repetitive financial operations. And for many enterprises, it's already delivering. The efficiency gains are real.

But there's a problem that most organizations haven't confronted yet. The controls they have in place were never designed for this.

The Assumption Built Into Every Enterprise Spend Control

Every expense management platform, every corporate card program, every AP workflow tool on the market shares a common design assumption: a human is making the spending decision.

This assumption is so fundamental that it's invisible. It shapes everything — from how approval workflows are structured to how audit trails are generated to how policy violations are flagged.

Approval workflows require a manager to click "approve." That works when the requester is an employee waiting for sign-off. It doesn't work when the requester is an AI agent that has already executed the transaction by the time the approval email arrives.

Spend limits are enforced through soft controls — monthly card limits, per-diem caps, category restrictions communicated in policy documents. These work when the spender reads the policy and exercises judgment. They don't work when the spender is a model that has the policy encoded in a system prompt and no hard technical constraint preventing it from exceeding the limit.

Reconciliation and audit happen after the fact. Finance reviews the expense report on Tuesday for what happened over the weekend. For human employees, this lag is acceptable — the spend volume is bounded by human pace. For AI agents operating continuously, by Tuesday the agent may have made thousands more transactions.

The gap isn't a gap in intent. The tools exist because they work. The problem is that AI agents with spending authority are a genuinely different kind of actor — and they expose the structural limits of controls designed for human-speed, human-judgment spending.

What "Agentic Payments" Actually Means

Agentic payments is a term emerging to describe transactions initiated by autonomous AI systems acting on behalf of an organization. It's distinct from automated payments (scheduled, rule-based, deterministic) and from human-initiated payments (online checkout, expense submission, wire transfer).

Agentic payments are neither. They're dynamic. The agent assesses a situation, determines that a purchase is appropriate, selects a vendor, determines an amount, and executes — without a human making any of those individual decisions. The human authorized the agent to operate. They didn't authorize each spend.

This matters because the risk profile is different.

With a scheduled automated payment, you know exactly what will happen before it happens. You configured it. With an agentic payment, you know the agent's general mandate and objectives, but the specific transaction is the agent's decision. That introduces a new class of risk: not fraud, not error, but autonomous action that's outside the intended scope of the agent's authority — executed at machine speed, potentially at scale.

Consider a few scenarios that are happening right now in enterprises deploying agentic AI:

A SaaS procurement agent is tasked with ensuring no subscription lapses. Over a long weekend, it identifies 23 subscriptions approaching renewal dates and renews all of them — including three vendors whose contracts are under legal review and two that finance flagged for cost optimization last quarter. Nobody told the agent. The agent had no way to know. By Monday, $180,000 has moved.

A travel booking agent is configured to optimize for cost and availability. It books a flight and hotel at rates that technically fit within the policy as written — but uses a non-preferred vendor, creating a compliance issue with a separate partner agreement. The agent wasn't wrong. The policy didn't cover this.

An expense automation agent processes vendor invoices automatically. One vendor submits a duplicate invoice for a payment already made. The agent, lacking context from a separate accounting system, approves it. The duplicate payment goes out before the next reconciliation cycle catches it.

None of these are AI failures in the technical sense. The agents did what they were designed to do. The failures are control failures — the absence of an enforcement layer that could have evaluated each transaction against a policy and stopped the ones that shouldn't have happened.

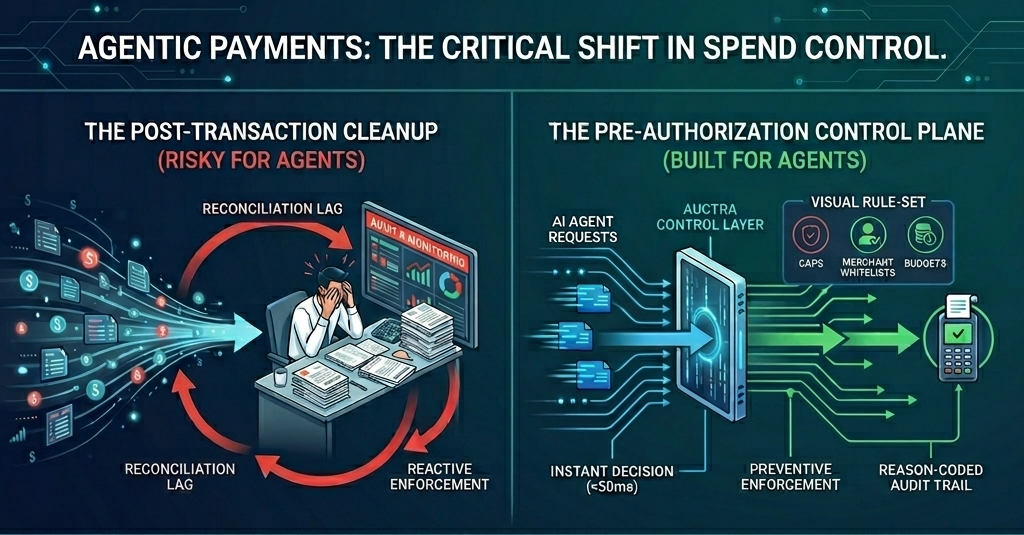

Why Post-Transaction Controls Fail Agentic AI

The instinct many organizations have when facing this problem is to add more monitoring. Better dashboards. More granular expense reports. Faster anomaly detection.

This is the wrong instinct, for one fundamental reason: post-transaction controls cannot prevent a transaction that has already occurred.

When an AI agent executes a payment, money moves. The merchant is paid. The card is charged. A purchase order is cut. What happens after that — the review, the flagging, the potential reversal — is damage control. It is not spend control.

For human employees, post-transaction controls are tolerable because the volume and velocity of human-initiated spend is bounded. A person can only submit so many expense reports. The anomalies are discoverable at the pace finance teams can handle.

For autonomous agents, post-transaction controls are structurally insufficient. An agent operating continuously can generate spend volume that outpaces any human review process. By the time an anomaly is flagged, the pattern may have repeated hundreds of times.

Monitoring tells you what happened. It doesn't stop what should not have happened.

What Pre-Authorization Infrastructure Looks Like

The alternative model — and the one that actually works for agentic payments — is pre-authorization: evaluating every spend request against a defined policy before funds move.

This is not a new concept in payments. Card networks have always had an authorization layer. When you swipe a card, the merchant's terminal sends an authorization request to the card network, which checks it against the issuer's rules and returns an approve or decline in milliseconds. The purchase only goes through if the authorization passes.

What's new is applying this model explicitly to AI agent spend — and making the policy layer programmable, configurable, and visible to the organizations deploying agents.

In a pre-authorization model for agentic payments, the enterprise defines a spending mandate: a structured set of rules that governs what an agent is permitted to spend on, with whom, for how much, and when. This might include:

- Merchant category codes (MCC): The agent may only transact with merchants in specific categories — software subscriptions, travel, office supplies. Transactions at uncategorized or out-of-scope merchants are declined.

- Merchant allowlists and blocklists: Specific vendors may be explicitly permitted or blocked, regardless of category.

- Per-transaction caps: No single transaction may exceed a defined dollar amount.

- Aggregate limits: The agent's total spend may not exceed a monthly or quarterly budget.

- Time restrictions: The agent may only transact during business hours, or may be blocked from operating on certain days. When the agent initiates a spend, the authorization request goes through the policy layer first. The system evaluates the request against the mandate and returns an APPROVE or DECLINE — with a reason code — before any funds move. The agent receives the decision and acts accordingly. The entire evaluation happens in under 50 milliseconds.

This approach has several properties that post-transaction monitoring cannot replicate. It is preventive rather than reactive — the problematic transaction never happens. It is reason-coded — every decision, approve or decline, is logged with a specific explanation, creating an audit trail that is built into the process rather than reconstructed afterward. And it is instant — the enforcement happens at machine speed, appropriate for the agents it governs.

What Enterprise Teams Should Be Asking Right Now

If your organization is deploying AI agents with any kind of spend authority — or planning to — the questions worth asking are specific:

Where is the hard enforcement layer? Not the policy document, not the system prompt, not the monitoring dashboard. The technical layer that makes an APPROVE or DECLINE decision before funds move.

What happens if the agent acts outside its intended scope? Can you terminate a specific agent's spending authority instantly? Can you freeze a class of instruments? Is there a kill switch that works in seconds, not hours?

What does your audit trail actually capture? Can you reconstruct, for any transaction, exactly which policy rule governed the decision, what the agent's request contained, and what the authorization response was?

What is your rollout path? Moving directly from no controls to full enforcement carries risk. A safe rollout pattern starts with observation — logging what would have been blocked without blocking it — before enabling enforcement.

These aren't hypothetical questions. They're the operational requirements for any enterprise that wants to deploy agentic AI responsibly on financial workflows.

The Control Plane for Agentic Payments

Auctra is real-time spend control infrastructure built specifically for this problem. It sits between your policy and any AI agent that tries to spend, evaluating each authorization request against your defined mandates and returning a decision — with a reason code — in under 50 milliseconds. Pre-fund. Before money moves.

It integrates with existing card issuing infrastructure via a simple REST API. Organizations can start in Observe mode — auditing agent spend patterns against policy without blocking anything — and move to Enforce mode when ready. A kill switch on any agent, instrument, or policy takes effect immediately.

The problem of agentic payments isn't going away. The volume of autonomous AI spend will grow as more organizations deploy agents across their financial operations. The organizations that build the control layer now — before the incidents, before the audit findings, before the regulatory attention — will be in a fundamentally better position than those who treat it as a problem to solve later.

Post-transaction reconciliation was never a control strategy. It was always a cleanup strategy. For agentic payments, the cleanup comes too late.

Ready to see how Auctra works? Talk to us or explore the documentation.